Your Financial Health Score: What It Is and How to Improve It

What your financial health score means, what each tier looks like, and how to improve it. Free quiz included.

Most people have a rough sense of how they're doing financially. You know if things feel tight. You know if you're saving or not. But "rough sense" and "actual picture" are surprisingly far apart.

I tracked my own spending for over 5 years. 4,600+ transactions. And for most of that time, I was just recording. Not really doing anything with the data. I knew where my money went, but I didn't know which parts of my financial setup were actually costing me. Tracking doesn't automatically mean fixing. Those are two different things.

A financial health score closes that gap. It takes the vague feeling of "I think I'm doing okay" and turns it into a number. Not a credit score. Not a net worth figure. A measure of whether your financial foundations are solid or quietly leaking.

What Is a Financial Health Score?

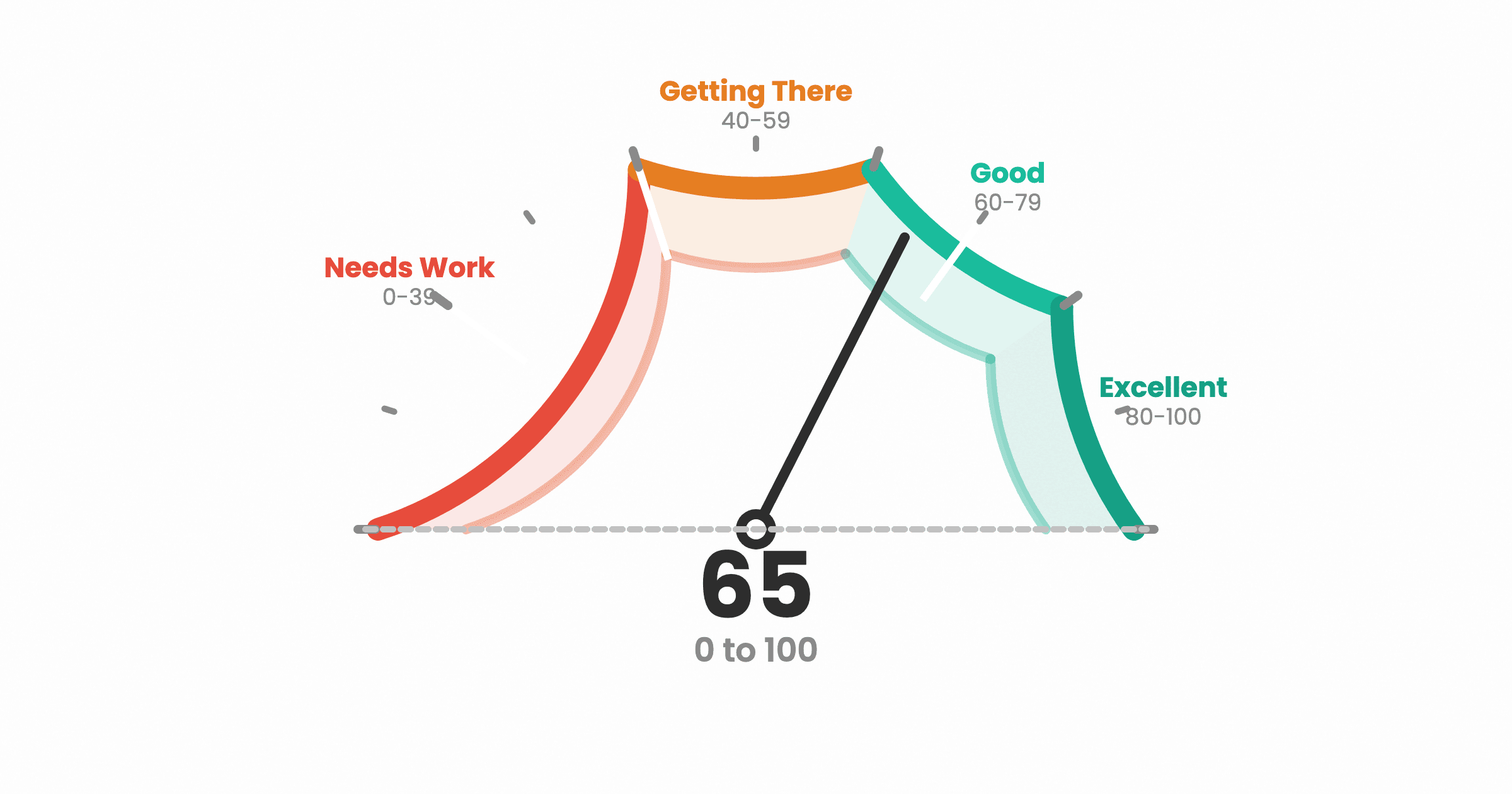

A financial health score is a single number, 0 to 100, that measures how well your core financial systems are working. Not how much money you have. How structurally sound your setup is.

Think of it like a building inspection. A building can look fine from the outside but have foundation cracks, missing insulation, or faulty wiring. A financial health score checks the structural stuff: Do you have a spending plan? An emergency fund? Are you collecting your employer match? Is high-interest debt eating your progress?

The score is built on the Leak Ladder, which identifies 9 financial leaks. Each leak is something in your financial setup that's quietly costing you money, security, or progress. Your score reflects how many of those leaks you've plugged and how much progress you've made on the ones that are still open.

Someone with no debt, a full emergency fund, and retirement savings on track will score high. Someone with no spending plan, no emergency fund, and credit card debt will score low. Most people are somewhere in the middle, with 3-5 leaks they didn't know they had.

How the Score Works

Three things to know:

Foundational leaks matter more. Not having a spending plan or an emergency fund affects your score more than not investing beyond retirement. The score reflects the Leak Ladder priority order: the lower rungs have more impact on your score because they protect everything above them.

You get credit for progress. You don't have to fully resolve a leak before your score starts moving. If you're halfway through paying off high-interest debt, the score reflects that. Every dollar of progress counts.

Paused leaks don't count against you. Some leaks get paused because there's something more important to handle first. For example, retirement savings is paused while you still have high-interest debt (because the debt costs more than investing would earn). Paused leaks don't drag your score down. They're just waiting until you're ready for them.

What Each Tier Means

| Score | Tier | What It Means |

|---|---|---|

| 80-100 | Excellent | You're in great shape. Your financial foundations are solid. Most or all of your leaks are plugged. Keep doing what you're doing. |

| 60-79 | Good | You're doing well. The big stuff is mostly handled, but there are a few areas to tighten up. Usually 1-2 active leaks. |

| 40-59 | Fair | A few things to work on. You've got some foundations in place, but there are structural gaps costing you money or security. Usually 3-4 active leaks. |

| 0-39 | Needs Work | Let's get you on track. Several core leaks are open. The good news: plugging even one or two foundational leaks can move your score significantly. |

Most people land somewhere between 40-70 on their first check. That's normal. The score isn't a judgment. It's a starting point.

What Affects Your Score

Your score is determined by 9 financial leaks, listed here in Leak Ladder priority order. This order matters because each leak protects the ones above it. Fixing them out of order can undo earlier progress.

1. No Spending Plan The foundation. Without visibility into where your money goes, every other leak is invisible. A spending plan doesn't have to be complicated. It just means knowing where your money goes each time you get paid.

2. No Starter Emergency Fund Less than $1,000 saved for emergencies. This is the buffer that keeps one car repair from turning into new debt. It's small on purpose: just enough to prevent backsliding while you handle higher priorities.

3. Missing Employer Match / Super Not Tracked In the US: your employer offers to match retirement contributions and you're not taking the full match. That's free money left on the table. In Australia: your super is mandatory, but if you've changed jobs, you might have multiple accounts quietly draining fees. The leak is about tracking and consolidating.

4. High-Interest Debt Any debt at or above 7% APR. Credit cards, personal loans, buy-now-pay-later. This is one of the most impactful leaks because it actively works against everything else. While it exists, it compounds against you. Every dollar you invest while carrying 18% credit card debt is a dollar that would do more work paying off the debt.

5. No Full Emergency Fund 3-6 months of essential expenses saved. This is the real safety net. Without it, a job loss or medical emergency sends you back into debt. This leak only appears after high-interest debt is resolved (before that, you get the starter fund leak instead).

6. Other Debt Debt below 7% APR. Student loans, car loans, lower-rate personal loans. Not an emergency like high-interest debt, but still a hole in the bucket. Whether to aggressively pay it down or invest instead depends on the rate and how much it's stressing you out.

7. No Savings Goals No defined savings targets with amounts and timelines. This leak is unique: it's never paused. You can work on savings goals at any point, even while handling debt. Because savings goals are about building the life you want, not just fixing what's broken.

8. Not Saving Enough for Retirement Total retirement contributions (including employer match or super) below 15-20% of gross income. This leak is paused if you have high-interest debt, because the debt costs more than what investing would return.

9. Not Investing Beyond Retirement No brokerage accounts, index funds, or other investments outside retirement accounts. This is the top of the ladder. It's paused until the emergency fund, high-interest debt, and retirement leaks are all resolved.

How to Improve Your Score

The fastest path is to fix leaks in Leak Ladder order, starting from the bottom and working up.

Why that order? Because the leaks that affect your score most tend to be the foundational ones. And the foundational leaks protect the ones above them. Investing while carrying credit card debt is a net loss. Building wealth without an emergency fund means one surprise expense pulls everything down.

Here's the practical version:

If you score 0-39: Focus on the first three rungs. Get a spending plan running on your pay cycle. Start building a $1,000 emergency fund. Check your employer match or super situation. These three are some of the highest-impact leaks you can fix.

If you score 40-59: You probably have the basics but one or two structural issues are dragging you down. High-interest debt is the most common culprit at this tier. Attacking it aggressively (avalanche or snowball method, your call) will move the needle fastest.

If you score 60-79: You're in good shape. The remaining leaks are usually the upper-ladder items: full emergency fund, retirement optimisation, savings goals. These take longer to resolve but they're the difference between "doing well" and "financially solid."

If you score 80-100: Your foundations are set. From here it's about maintaining what you've built and letting compounding do its work.

The score updates as you make progress. You don't have to fully resolve a leak before seeing improvement. Paying off half your high-interest debt? Your score reflects that. Saving $500 toward your $1,000 emergency fund? That progress counts too.

How Often It Updates

In the app: Your score recalculates every pay cycle based on your actual transactions and progress. As you log spending, pay down debt, or hit savings targets, the score adjusts automatically. It's a living number, not a one-time snapshot.

From the quiz: The Know Your Digits quiz gives you a snapshot based on your answers at that moment. about 3 minutes. It detects which leaks you have and calculates your score.

The quiz and app scores should be close, usually within 0-8 points of each other. The small difference exists because the app tracks exact dollar amounts (so it can calculate precise progress on each leak), while the quiz uses broader answer tiers. Same ballpark, slightly different precision.

Find Your Score

If you've read this far, you probably want to know where you actually stand.

The Know Your Digits quiz takes about 3 minutes. It asks questions about your financial setup, detects your leaks, and gives you your score with a breakdown of what to fix first, in order.

No account needed. No bank login. Just honest answers.

Once you know your score, the Leak Ladder guide walks through each rung in detail: what each leak is, why the order matters, and when certain leaks get paused while you handle the ones below.

Go Deeper

- The Leak Ladder: The Complete Guide: the full 9-rung priority system

- You Don't Have a Savings Problem. You Have a Leak.: what leaks are and why they matter

- The Emergency Fund Lie (And What Actually Protects You): starter vs full fund

- The Debt Payoff Order Nobody Talks About: avalanche vs snowball, and why order matters

- Why Budgeting Apps Fail (And What Should Replace Them): the 3-week wall and what works

Joy Casfhir

Accountant turned app builder. Tracked 4,600+ transactions by hand over 5 years. Had all the data but no system for knowing what to fix first. That experience became the Leak Ladder: your money has leaks you can't see, and there's an order to fixing them. Built YourDigits to find those leaks and tell you what to fix first.

@casfhirCurious which leaks you have?

The Know Your Digits quiz takes 3 minutes and shows you which of the 9 leaks are yours, in priority order.

Find my leaks